Back-of-the-envelope cost calculation of "zero COVID"

"The first-mover advantage in recovery is in line with economic intuition."

This is a translation of 关于“零容忍”防疫政策成本的估算 Estimate of the policy cost of “zero COVID”, by 王丹 Wang Dan, 恒生中国首席经济学家 chief economist of Hang Seng Bank China. It was first published on FT中文网 FTChinese.com on December 20, 2021, with the note that it reflects only Wang’s/her personal views.

***

关于“零容忍”防疫政策成本的估算 Estimate of the policy cost of “zero COVID”

文 | 恒生中国首席经济学家 王丹

By Wang Dan, Chief Economist of Hang Seng Bank China.

As many countries relaxed the control measures over COVID-19, the world is closely watching the developments in China. Up to now, China still insists on the “Zero COVID” policy, which includes restrictions on cross-border travel, the “14+7” (days) quarantine, lockdown of pandemic-stricken residential compounds, and other local measures.

Many foreign companies have complained because many of their production activities relied upon foreign experts who came to China to test and upgrade machines, and senior corporate officials based overseas usually would need to come to China to negotiate with Chinese suppliers personally.

From a higher-level perspective, the “zero COVID” policy disrupted port services and business operations and played havoc with the accommodation and catering industry as well as consumption.

However, if the pandemic runs out of control, the impact on the economic and social order may be even more unbearable. We have estimated the gains and losses of the pandemic control policy from the standpoint of economic efficiency. The results show that in 2021, the output of the industrial, agricultural, and financial sectors expanded faster than the historical growth rate. The impact of the “zero COVID” policy is concentrated in the accommodation and catering industry, but because their added value merely accounts for three percent of the service sector, the impact on the overall economy is limited. The real estate sector contracted by nearly five percent compared with the historical growth rate, but this was not caused by COVID-19 but was the intended result of deleveraging.

A back-of-the-envelope estimate

We estimated the impact of pandemic control measures based on the historical growth rate. We first calculated the average annual GDP (Gross Domestic Product) growth rate of the primary industry (agriculture), the secondary industry (industrial and construction sectors), and the tertiary industry (services) from 2016 to 2019. We used the GDP at the constant price in 2016 to remove the effects of inflation. The four-year average was used as the trend value to calculate the GDP in 2020 and 2021, which could be interpreted as “GDP in case there was no pandemic”. The nominal GDP published by the National Bureau of Statistics (also converted to the 2016 constant price) minus the trend value is the difference caused by the impact of the pandemic.

If the premises and assumptions are changed, there will be different figures, but the absolute value of the number is not important. What is important is the relative size and development direction. Even if different years are used to calculate the trend, or other conditions are changed, our conclusion still stands.

The National Bureau of Statistics has published the statistics for the year 2020. (On December 17, 2021, the Bureau of Statistics also published the final, verified data. The sub-indices were slightly adjusted, but it does not affect our calculation results). The conclusion is obvious: The pandemic in 2020 lowered the output of all sectors. The GDP in the agriculture sector, the industrial sector, and the service sector declined by 7 percent, 3 percent, and 11 percent respectively. It should be noted that these differences include the impact on productivity by COVID-19, the impact of pandemic control measures such as lockdowns, increased overseas demand for China’s exports, the stimulus policies, changes in consumer habits after the pandemic (such as teleworking and avoiding crowded public places) and so on. It is difficult to tell one of them from another in the numbers.

It is a bit more complicated to perform the calculation for 2021 because data on the economy is only available for the first three quarters. As a result, the GDP of the entire year has to be first estimated. In 2021, production in the industrial sector has basically returned to the level before the pandemic. Therefore, it is possible to use the GDP numbers in the first three quarters of 2019 - their share of the 2019 total, to be exact - to estimate the 2021 GDP, and then compare the number to the historical growth rate. The year 2021 is different from 2020 because relatively fewer people were infected with COVID-19, which had a lesser impact on productivity. There were no extra stimulus measures in terms of monetary and fiscal policies, and the actual policy support is weaker than that in 2020. Therefore, this difference reflects the joint impact from the “zero COVID” policy, the macro policies, and other factors. The conclusion is therefore meaningful.

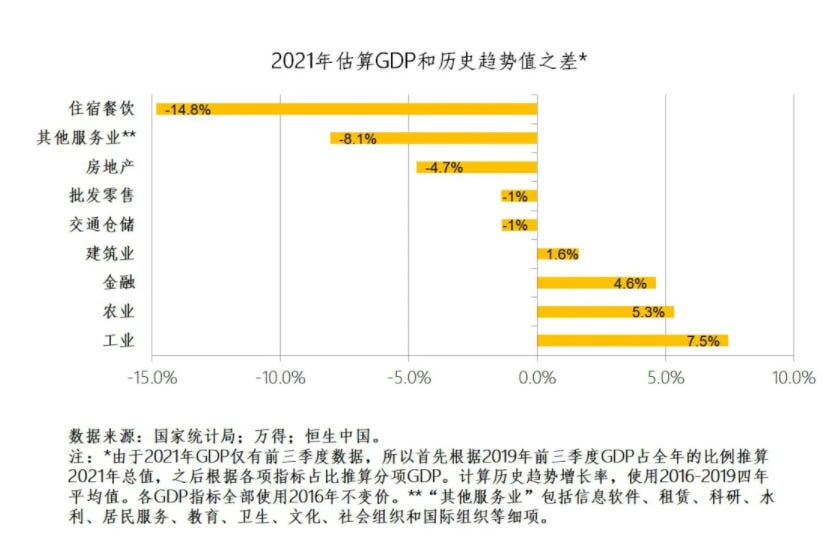

The added value of agriculture and industry was higher than the historical trend. Industrial added-value was eight-percentage higher, ranking best among all sectors. Added-value in agriculture and construction was five-percentage and two-percentage higher, respectively. In normal years, the primary, secondary, and tertiary industries usually account for seven percent, 39 percent, and 53 percent of GDP. Following the logic, the GDP in 2021 was one percent higher than the historical growth rate, with export being the greatest driving force.

As other countries failed in containing COVID-19, they needed to rely on Chinese manufacturing, which boosted industrial production and exports. In terms of industrial added value, the manufacturing sector accounts for as high as 85 percent, and many segments have a long industrial chain. Absent strict control of COVID-19, manufacturing output could have exceeded the pre-pandemic volume due to exports, but the increase would have been limited. The biggest benefits of the strict control were to avoid the interruption of production and transportation, maintain the integrity of the industrial chain, and stabilize market expectations. Agricultural activities are generally labor-intensive and season-sensitive, with a reliance on transportation and professional services (such as the logistics of fertilizer and feed, the prevention of animal diseases, and so on). Strictly curbing the spread of COVID-19 was crucial to ensuring agricultural production, which was the prerequisite for China’s agricultural output to reach an all-time high in the pandemic.

The pandemic’s largest negative impact is concentrated in the service industry, but a distinction needs to be made in this regard. First, not all services contracted. For example, the added value of the financial sector is nearly five percent higher than the historical growth rate as a result of the development of the capital market and financial opening-up. Both wholesale and retail as well as transport and warehousing have contracted slightly, but the retail and logistics related to e-commerce have greatly expanded, while the contraction concentrated on the retail market in small cities and rural areas.

Second, the contraction in services was not solely due to COVID-19. Because a significant part of the services actually correlates with real estate and infrastructure, China’s efforts to deleverage in these two areas have resulted in a decline in related added value. The added value of real estate is nearly five percent lower than the historical growth rate.

Third, the accommodation and catering industry bore the full negative force of “zero COVID”, with the added value 15 percent lower than the historical growth rate). However, because the added value of the accommodation and catering sector only accounts for three percent of the total service sector, the impact on the economy as a whole is extremely limited.

Compromise between efficiency and fairness

The strict control of COVID-19 bought direct inconvenience to daily life. However, as explained above, we cannot draw the conclusion that “zero-COVID dragged the overall economic recovery”. On the contrary, it seems that the first-mover advantage of China’s economic recovery comes from the control of the pandemic. This conclusion is in line with economic intuition. As the global industrial chain was shaken, China, being the first to bring COVID-19 under control, ensured supply at home and abroad as well as employment. Granted, opening borders would boost the service industry, but the impact on domestic production, life, and the hospital system may be immeasurable.

However, strict control measures have indeed exerted a lasting impact on the numerous small and micro enterprises as well as the individual business household, many of which are in the service sector. In particular, in the second half of 2021, tourism and business travel are still frequently subject to control measures, which have a great psychological impact on consumer behavior. This is why liquidity problem occurs in small and medium-sized enterprises to varying degrees.

The downturn in the real estate market aggravates the situation because if families in small and medium-sized cities do not buy a new apartment, they usually wouldn’t buy big-ticket items such as cars or air-conditioners. Even for the industrial sector which benefits from “zero COVID”, businesses that cannot effectively curb costs (mostly small and medium-sized private enterprises and individual business households) will be on the verge of survival.

Since the global outbreak in March 2020, China’s biggest growth engine has been exports, which bolstered external demand-oriented industrial production. Exports have been fluctuating at an all-time high for several months, and the room for further growth next year is limited. Industrial production may face the pressure caused by a slowdown, and the engine of economic growth has to shift, at least partially, to services.

Recent policies have put more emphasis on supporting companies in the service sector, including loan extension for small and micro enterprises, tax relief, and fee reductions. However, the fundamental solution lies in expanding domestic demand. Consumption is still the stumbling block to domestic economic recovery. As the consumption function suggests, consumer spending is mainly determined by income, it will be difficult to increase income within a short period of time. The most direct and effective approach is to directly issue cash subsidies to low- and middle-income groups. The digital currency launched by the central bank was recently piloted in Luohu in Shenzhen and other places. Digital “red envelopes” were issued to the public, with the condition that the money shall be used for consumption at designated merchants within a specified period. The recently concluded Central Economic Work Conference stressed that next year’s economy will focus on “stability”. Direct subsidies to consumers may be the most effective approach to stabilize economic growth. Therefore, we expect wider coverage and more application scenarios of the digital currency next year. (Enditem)