China’s central bank won't budge on face-to-face requirement for opening of most essential accounts

Brick-and-mortar sites retain an edge. Big Tech-backed Internet-based banks would have to wait.

Highlights:

1) China’s banking regulator sticks to the on-site human-supervised opening of the most important type of bank accounts, where some voices including a former top financial official publicly called for relaxation;

2) Larger banks with more physical presence retain their edge in this, while smaller and especially emerging, tech-savvy banks will have to make do with limited physical branches or none at all;

3) Despite being limited to provide less-comprehensive accounts to customers, Internet-based banks such as WeBank have already made a mark. But what if the Chinese regulator changes mind one day?

4) The banking regulator effectively said there are enough banks in China already. To me, that suggests increased difficulties in securing new banking licenses in the future.

***

The People’s Bank of China’s standing regulation in 2016, and a subsequent amendment in 2018, of bank accounts for individuals 个人账户, divide them into three categories: Type I, II, and III.

Type I is the most essential bank account. Individuals can do whatever they want out of Type I accounts - depositing and withdrawing cash, make investments (e.g. buying what the Chinese call wealth products 理财产品), transfer money, paying bills, and payment - with the least regulatory hurdles.

The uses of Type II and Type III accounts are more limited, with stricter regulations.

For example, a Type II account can be used as a savings account and for investment. But if it is not tied to 绑定 a Type I account, the transfer in and out of a Type II account is capped at 10,000 yuan a day and 200,000 yuan a year. (1 USD= 6.53 Yuan)

Type III account is aimed at the most frequent and digital uses like paying for groceries in a supermarket, online shopping, paying the electricity bills digitally. The regulatory requirement is, even more, stricter - the balance on a Type III account must NOT exceed 1,000 yuan at any given time, and payment out of it must not exceed 5,000 yuan a day or 100,000 yuan a year.

Therefore, despite the highly frequent use of Type II and Type III accounts, Type I remains the crown’s jewel for banks - that’s where the individuals’ chunk of money remains, as the savings for a bank to loan out later.

So far, and perhaps as a consequence, the opening of a Type I account has to be done face to face (including done at a machine with the supervision of a human on-site). Type II and Type III are allowed to be opened digitally - such as uploading an ID card picture and confirming via a text message to a mobile phone number, away from a brick and mortar branch.

Earlier this year, Wang Tianyu 王天宇, head of Zhengzhou Bank 郑州银行, out of the provincial capital Zhengzhou City in Henan Province, sought to have the rule governing Type I relaxed.

Wang’s initiative is representative of smaller banks’ urgent needs to attract individual clients, which has been hindered by the very limited number of physical branches - since the regulator mandates Type I accounts must be opened on-site.

ICBC, one of the largest state-run banks, has 15,529 grass-root branches in China by the end of 2019, according to its annual report. The smaller but also nationwide banks - what the Chinese call joint-stock banks 股份制银行 - like China Merchants Bank and China Everbright Bank are, respectively, below 2,000 in branches and they are already the big guys in the league. Imagine the midgets (no disrespect).

Now, these shorter guys can out-innovate, outsmart and out-service the Big Four in numerous ways, but will probably never match them in brick and mortar branches.

Perhaps with this in mind, Wang, in his capacity as a deputy to the National People’s Congress 全国人大代表 submitted a recommendation 建议 during this year’s session of the NPC, China’s national legislature. As a routine in processing similar recommendations, the NPC relays his recommendations to competent authorities - in this case, the CBIRC.

It’s also worth noting that Xiao Gang 肖钢, the former head of China securities regulator China Securities Regulatory Commission, also weighed in on the issue in an article published in May on China Finance 中国金融, a magazine under the PBOC, the central bank, advising to allow the digital opening of Type I accounts for small businesses and individuals.

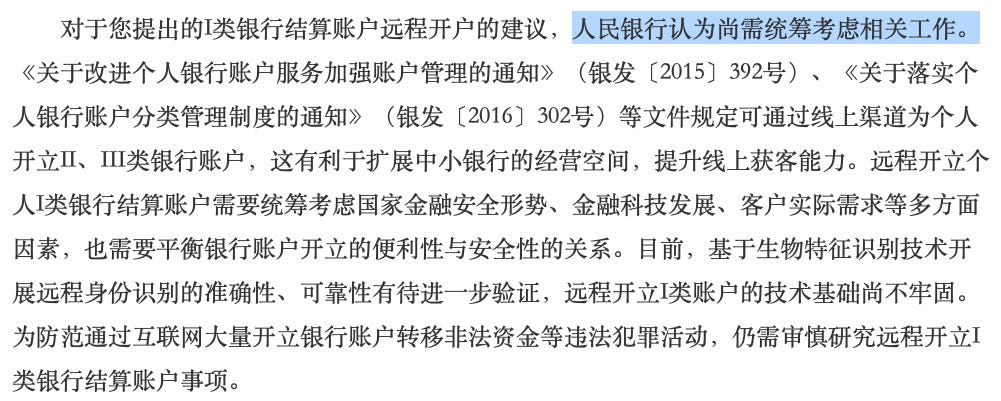

On Sept. 4, the banking regulator responded to Wang’s recommendation (but media reports of the response only surfaced around Nov. 26), citing the PBOC as saying the permission of allowing opening Type I accounts digitally needs to be coordinated and conducted comprehensively, effectively a rejection.

The reasoning for the rejection is elaborated below. Forgive me for being unable to tell if it is attributed to the PBOC or the CBIRC, because of the wording:

The remote opening of personal Type I bank settlement accounts requires overall consideration of the national financial security situation, the development of financial technology, the actual needs of customers, and other factors, as well as the need to balance the convenience of opening bank accounts with security. At present, the accuracy and reliability of remote identification based on biometric identification technology need to be further verified, and the technical basis for remote opening of Type I accounts is not yet solid. In order to prevent illegal activities such as transferring illegal funds through the Internet by opening a large number of bank accounts, the remote opening of Type I bank settlement accounts still needs to be carefully studied.

Now that the facts have been established, below is a few observations that are mainly aimed at stimulating your thoughts on this matter:

1) With tech innovations emerge every day, the reasons for maintaining physical banking branches are dwindling, just as people are turning away from post offices to the Internet for communication. For example, ICBC’s annual report said its branches - both within and outside China - decreased by 215 to 16,605 in 2019. Chinese media also reported closures of physical banking branches.

But the on-site opening of Type I accounts, as mandated by standing regulations, is perhaps one of its last irreplaceable uses.

However, the falling role of physical branches seems irreversible, unless banks can somehow figure out revolutionarily better uses for them. Absent that, the branches will go increasingly from an asset to a liability, which may also affect the thousands of men and women that currently staff them.

2) If the requirement is scuttled one day, which banks benefit most, and which ones are likely to lose out from that change?

The landscape of Chinese banking isn’t what it used to be these days. Eighteen private capital-backed banks, including Big Tech-backed Internet-based ones, have sprung up, according to the CBIRC, which now believes, effectively, China has enough number of banks (paraphrasing its words:大家普遍认为,在现有的银行服务体系中银行数量已基本不是或不是主要问题 It is generally agreed that the number of banks is no longer a problem, or not a major problem.)

Basically, Chinese banks may roughly fall into one of the three following categories:

A. Those already established nationally with a wide network of physical sites, headed by the Big Four and followed by China Merchants Bank, China Everbright Bank, etc.

B. Those emerging but so far largely local banks which usually carry the home province of the home city in their names, like the one Wang headed in Zhengzhou, with considerable local physical presence but little to none outside its home;

C. Those just breaking ground, backed by private capital - in particular, Big Tech - with minimal physical presence but enormous tech advantages.

My theory is, ironically, if Wang’s recommendation were to be adopted, it’s going to be the kind of bank that he heads that’s gonna get burnt. The Big Four are already nationally established with a huge customer base, and their size affords them some buffer space to adapt and even take a few hits.

But the largely-local banks? I can’t help but think the Internet traffic that Ant Financial could direct to its MYbank or WeChat to its WeBank will just eat them alive.

Following this logic, the banking regulator may have done Wang a favor by rejecting his recommendation.

3) As of now, the newest tech-savvy banks, operate out of the Type II accounts that customers open with them. For example, Tencent-backed WeBank said the overwhelming majority of individual bank accounts opened at this bank by customers are Type II accounts.

Even so, they have made some inroads. WeBank said in its 2019 annual report that its effective individual customers amount to 200 million at year’s end, and one particular loan product 微粒贷 had been used by 28 million individuals from 2015 to the year’s end.

What if their hurdle to Type I accounts is cleared in the future? Well, by Alipay and WeChat Pay crushing China Unionpay and the card payment industry, I think Ant Financial and Tencent have already shown their muscle.

Thank you for reading. Welcome to subscribe and share!