How Local China Built the EV Boom

A new study challenges the story of Beijing-led industrial policy, tracing how local governments and private firms reshaped the auto industry from below.

China’s electric-vehicle industry has become one of the most contested stories in the global economy. To some, it is a textbook case of successful industrial policy. To others, it is a story of subsidies, overcapacity, brutal price wars, and unfair competition, now spilling into trade disputes with the U.S. and Europe.

for export and containers sitting at a port in Shanghai")

A newly published paper offers a more nuanced explanation. In “The Rise of China’s Electric Vehicle Industry: Strategic Alliances Between Local Governments and Private Capital,” published in the July issue of The China Journal in 2026, Fengming Lu and Xiao Ma argue that China’s EV boom was driven in large part by alliances between ambitious local governments and agile private firms, which repeatedly found ways around tight central regulations—a dynamic that produced both China’s spectacular EV successes and many of its costly failures.

Fengming Lu is a Lecturer (Assistant Professor) in the Department of Political and Social Change at the Coral Bell School of Asia Pacific Affairs, Australian National University. His research spans comparative politics and Chinese politics, with a particular focus on China’s political economy, industrial policy, local governance, and political selection.

Drawing on three decades of observation of China’s automotive sector, Fengming is currently working on a book project examining the rise of China’s EV industry. The project explores the interplay between central industrial policies, local governments’ developmental strategies, and global capital markets in shaping one of the most significant industrial transformations of the twenty-first century.

Xiao Ma is an associate professor of political science at the School of Government at Peking University. His research focuses on comparative political institutions, politics of development and Chinese politics. He is the author of Rethinking Political Meritocracy: An Attention-Based Approach (Cambridge University Press, 2026), and Localized Bargaining: The Political Economy of China’s High-Speed Railway Program (Oxford University Press, 2022). He received his Ph.D. in Political Science from the University of Washington.

With the authors’ permission, we are publishing a condensed excerpt from the paper below.

The Rise of China’s Electric Vehicle Industry: Strategic Alliances Between Local Governments and Private Capital (Excerpt)

Fengming Lu and Xiao Ma

ABSTRACT

This article challenges the prevailing view that China’s electric vehicle (EV) boom is primarily the result of top-down industrial policy. Drawing on the history of China’s automotive sector since the 1990s, it shows that stringent central regulations and entrenched state-owned enterprises (SOEs) excluded most localities from lucrative joint ventures. In response, local governments forged strategic alliances with private manufacturers, leveraging capital markets, policy loopholes, and post-2008 credit expansion to attract investment, upgrade industries, and diversify regional economies. These partnerships, initially in traditional automotive manufacturing, proved pivotal to China’s EV takeoff after 2015, enabling private firms to outcompete SOEs in innovation, responsiveness, and market expansion. Comparative cases in steel and pharmaceuticals illustrate the broader applicability of this dynamic. The study highlights the enduring adaptability of Chinese local governments and private capital in navigating central constraints, offering new insights into industrial policies, industrial upgrading, and local developmental states.

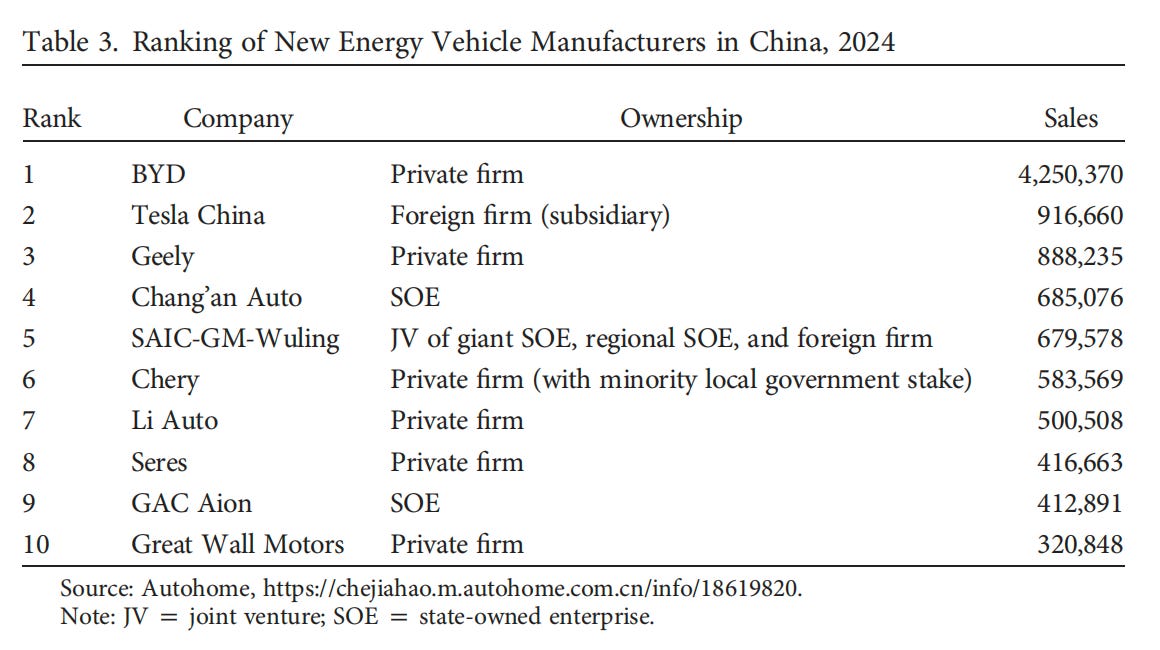

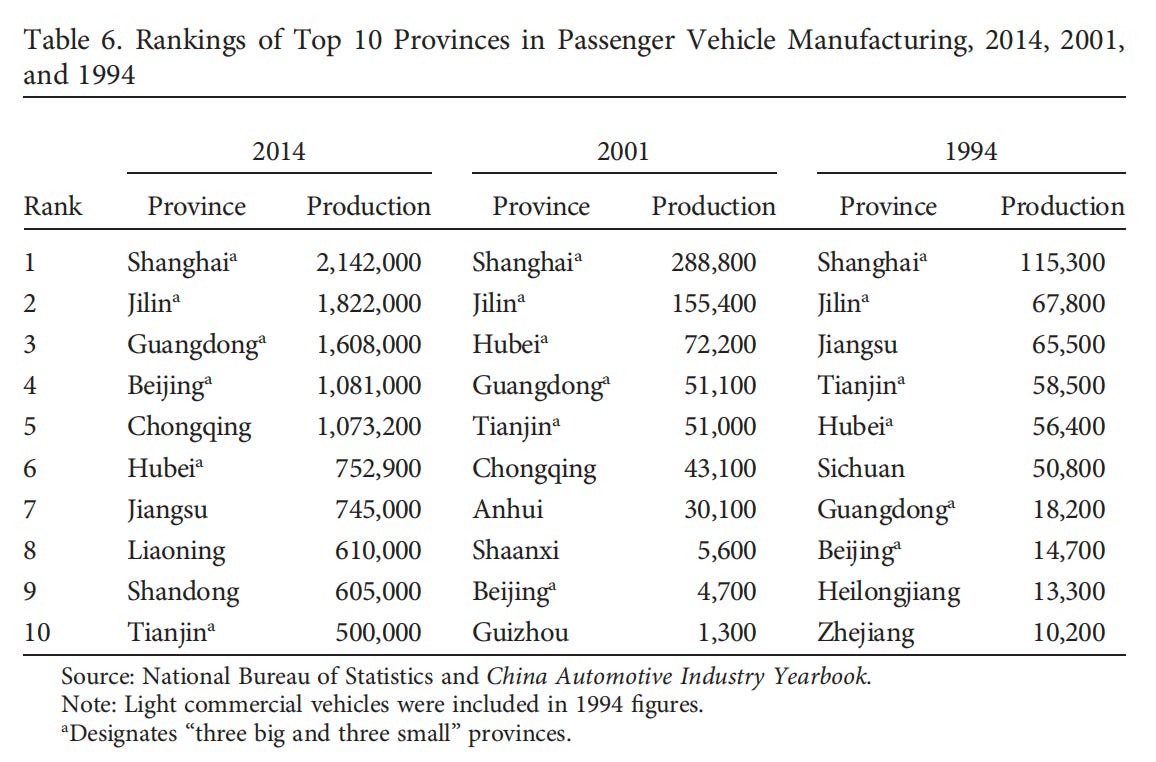

Since the mid-2010s, the Chinese automotive industry has undergone a profound transformation. Until then, the sector was dominated by joint ventures (JVs) formed between major foreign automakers and large Chinese state- owned enterprises (SOEs). Yet within a decade, China surprisingly emerged as the global leader in electric vehicles (EVs) and plug-in hybrid vehicles (PHEVs), collectively known as new energy vehicles (NEVs) in China, and rapidly closed the technological gap with the West in internal combustion engine vehicles (ICEVs), surpassing Japan to become the world’s largest exporter of passenger vehicles in 2023. This transformation ended SOE dominance in the sector. The leading NEV pioneers, NIO, XPeng, and Li Auto (known collectively as wei xiao li 蔚小理), are all private firms, alongside more established private automakers such as BYD and Geely, and new entrants such as Seres, Xiaomi, and Leapmotor. Among the 10 best-selling NEV marques in 2024, only three (SAIC-GM-Wuling, Chang’an, and GAC Aion) were SOEs or SOE-foreign JVs.1

The dynamics cannot be explained solely by central-level industrial policy or by the actions of local governments in isolation but rather by how local governments have responded to the central automotive industrial policy, particularly its stringent regulatory framework and bias toward SOEs, and collaborated with emerging private capital. The article argues that China’s EV boom, and the proliferation of both spectacular successes and costly failures, a phenomenon unmatched in the United States, Europe, or Japan, cannot be understood as top-down policy alone but as the unintended product of a triangular dynamic among central industrial constraints, local fiscal competition, and private capital’s agility. As we later demonstrate, this framework also illuminates patterns in China’s industrial development beyond automobiles, from traditional sectors such as steel and pharmaceuticals to cutting-edge industries such as AI.

THE 1990s: EMERGENCE OF ALLIANCES UNDER RESTRICTIVE INDUSTRIAL POLICIES AND FRAGMENTED PRODUCTION

The partnership between local governments and private automakers originated in the 1990s, well before China’s transition toward NEVs. Before China’s accession to the WTO in 2001, the country’s automotive sector was characterized by three defining features: high import tariffs on vehicles, an industrial policy favoring large SOEs, and a fragmented production landscape. The first two were embedded in the automobile industrial policies of 1987 and 1994.

Through the (in)famous “three big and three small” (sanda sanxiao 三大三小) policy [under which the state would support only three big and three small designated passenger-car producers], the central government strictly limited new entrants into the passenger vehicle market.2 Only models listed in the National Automobile Catalog, particularly its sedan subcatalog regulated by the Ministry of Machinery Industry and the National Economic and Trade Commission, could be legally sold nationwide.3 Meanwhile, passenger vehicle imports faced tariffs of 80–220 percent in the 1990s, shielding the designated SOEs from foreign competition. In line with broader SOE reforms, the state encouraged large automotive SOEs to form business groups (企业集团) and cultivate “national champions.” Additional preferential measures, including tax deductions, low-interest loans, and favorable access to foreign currency, were reserved for SOEs with annual production capacities exceeding 300,000 vehicles.4

Ironically, the industrial policy’s combination of limited domestic supply, given that many of the “three big and three small” were still struggling to ramp up production and raise domestic content, and high import tariffs spurred local governments to develop their own automotive industries. While most cities were formally excluded from large-scale passenger vehicle manufacturing, many already hosted small-scale producers, a legacy of Mao’s intentional economic fragmentation that accelerated through the early decades of the reform. Three waves of decentralization, the Great Leap Forward, the Cultural Revolution, and the fiscal decentralization of the 1980s, had encouraged provinces and prefectures to establish their own modest automotive works. Although often economically inefficient, these facilities alleviated chronic vehicle shortages under the planned economy, and many survived into the 1990s. In 1996, China had 130 automotive companies producing a total of just 1.48 million vehicles, with most firms manufacturing only a few thousand or fewer units per year. 5Industrial policy aimed to eliminate this lack of economy of scale by favoring large SOEs.

Although many local governments initially gained modest revenues from auto motive production, they were soon blocked by the central government from upgrading their industries. The industrial policy also maintained a prohibitively high entry threshold, 1.5 billion yuan in initial investment, for new carmakers until the 2010s. Localities without mass-production capacity therefore sought to attract licensed SOEs, but these efforts usually failed. SOEs resisted relocating core processes because of political ties with their home bases, the limited size of China’s auto market at the time, and structural asymmetries in central-local relations. Motivated by the promise of lucrative tax revenues from large-scale production in a protected market, local governments, especially at the prefecture level, turned to local state corporatism. Some established their own market-oriented automakers, while others partnered with township and village enterprises (TVEs).6 As privatization deepened in the late 1990s and early 2000s, this alliance advanced further: Many firms diversified their ownership structures, while latecomer cities allied with unlicensed private automakers to upgrade capacity. Together, these strategies laid the foundations for the enduring alliance between local governments and private capital in China’s auto industry.

THE PERIOD 2001–15: STRENGTHENED ALLIANCES UNDER THE DOMINANCE OF JOINT VENTURES

By the early 2000s, collaboration between local governments and private capital had already reshaped China’s fragmented automotive landscape. Yet the central industrial policy framework that constrained local ambitions in the 1990s remained largely intact. WTO accession in 2001 opened China’s market to foreign competition, but in practice the most lucrative opportunities still flowed to JVs set up between a handful of large SOEs and global automotive giants.

In this environment, emerging private automakers proved more willing partners for cities that had failed to secure successful JVs. BYD, which began automotive design and manufacturing only in the early 2000s, exemplified this trend. During its expansion, BYD partnered with numerous cities (many in central and western China), including Xi’an, Changsha, Fuzhou (Jiangxi), Hefei, Zhengzhou, Taiyuan, Dalian, Jinan, and Changzhou, offering substantial manufacturing investments in exchange for favorable local terms, including access to land, labor, and logistical support. To deepen ties, BYD established a dedicated division for urban rail transit, aligning with many cities’ infrastructure ambitions.7

Large SOEs remained far less flexible. BAIC, Beijing’s regional SOE, was China’s top EV producer between 2013 and 2019, even outselling Tesla globally in 2017. Yet BAIC’s strategy was narrowly aligned with Beijing’s priorities, focusing solely on EVs (to help the Beijing municipal government curb air pollution), totally giving up development of hybrid vehicles and producing mainly taxis and time-sharing vehicles, limiting its expansion elsewhere.8

Meanwhile, China’s integration into global capital markets, especially Hong Kong and New York, created new financing channels. One of the most notable cases was Geely’s 2010 acquisition of Volvo Cars from Ford for over US$1 billion, 10 times Geely’s 2009 annual profit. Denied financing by major policy banks—namely, the Export-Import Bank of China and China Development Bank, and the Bank of China—Geely secured only US $200 million from China Construction Bank’s Zhejiang branch, raising the rest through the global capital market and Chinese local governments. The Zhejiang-based automaker raised US$350 million from Goldman Sachs via Hong Kong, 6 billion yuan in loans from the governments of Chengdu and Zhangjiakou, and 4 billion yuan in equity from Daqing and Shanghai’s Jiading District. In return, Chengdu, Zhangjiakou, and Daqing, all seeking to upgrade into advanced manufacturing, secured Volvo vehicle or engine plants. Jiading, long known as “China’s Motor City,” diversified beyond Shanghai-Volkswagen to host Volvo Cars China.9

The Volvo acquisition illustrates how, even before the EV transition, the local government–private capital nexus enabled Chinese automakers to leapfrog in ICEV technologies. Through China Euro Vehicle Technology AB (CEVT), Volvo Cars transferred decades of know-how in design, engine and transmission systems, advanced driver assistance, and platform development to Geely. These developments laid the groundwork for the even deeper local government–private automaker partnerships that would define China’s EV boom in the late 2010s and 2020s.

AFTER 2015: NEW ENTRANTS PROLIFERATED THROUGH ALLIANCES

The proliferation of Chinese EV startups after 2015, driven by the technological shift toward electric and connected vehicles, further intensified the linkages between local governments and private automakers. Inspired by Tesla’s early success with the Model S, numerous Chinese entrepreneurs sought to replicate its achievements at home, leveraging the country’s rapidly advancing information and communications technology (ICT) sector and its increasingly sophisticated capital markets. 10In June 2015, the National Development and Reform Commission (NDRC) and the Ministry of Industry and Information Technology (MIIT) lowered entry barriers for EV manufacturers.11 The result was a wave of“internet-companies-turned-car-manufacturers” (互联网造车), in which hundreds of entrepreneurs, many with minimal automotive backgrounds, entered the sector, often backed by venture capital (VC) investors. This surge of new entrants shifted bargaining power toward local governments, enabling them to negotiate more favorable terms. As one official from an eastern city recalled, he received visits from dozens of EV startups in 2016 alone, including nearly all leading private EV manufacturers of the 2020s.12 Nanjing, long subordinate in its relationships with SAIC and Chang’an-Mazda, aggressively pursued EV opportunities and attracted five startups between 2016 and 2025.13

Yet key policy barriers remained. While it was easier to obtain approval from the provincial-level Development and Reform Commission, the most formidable was the requirement for “dual qualifications” (Shuang zizhi 双资质) from both the NDRC (for investment project approval) and the MIIT (for market entry). By 2019, only 15 carmakers had received NDRC approval, and just 12 had secured both qualifications, out of roughly 100 Chinese firms seeking to develop and manufacture EVs.14

An unintended loophole in the central-level industrial policy favored existing ICEV manufacturers: Any firm already licensed to produce ICEVs could obtain EV qualifications through a streamlined process. While designed to privilege large SOEs, this also elevated the value of regional auto manufacturers’ ICEV licenses, whether successful or struggling, and created new opportunities for local governments to connect them with private EV startups. One prominent case was NIO’s early collaboration with Hefei, in which the startup “borrowed” production qualifications from JAC, a struggling regional SOE. Although controversial, the practice was tacitly accepted after EV100, a think tank of former automotive regulators and SOE executives, persuaded the MIIT to relax enforcement.15 Subsequently, more EV startups followed this pathway to expedite their EV development and manufacturing.16 The collaboration across EV startups, regional carmakers, and local governments proved to be critical for the dramatic emergence of Chinese EV startups. This allowed NIO to become the first Chinese EV startup to mass-produce vehicles, delivering tens of thousands of units in 2018, well ahead of many domestic competitors and US peers such as Lucid and Rivian.

Before 2019, many private EV startups resisted taking equity investments from local governments, fearing interference in strategic decision-making. This changed dramatically in 2019–20. Sluggish post-trade-war sales in 2019 were compounded by the COVID-19 outbreak, which froze sales and financing for many startups. Stock market turmoil in March 2020 further depressed publicly listed EV firms’ stock prices. Local governments, flush with credit from the post-2008 credit expansion and eager to anchor EV production, stepped in.17 After missing a 10-billion-yuan deal with Beijing’s Yizhuang Economic and Technological Development Zone, NIO accepted a 7-billion-yuan equity investment from Hefei at a historic low in its stock price.18 The investment more than doubled in value within months, and Hefei’s success in securing NIO was celebrated by Chinese business media as the “Hefei Model” (hefei moshi 合肥模式). The precedent spurred a wave of high-profile local government investments through local government financing vehicles (LGFVs) in 2020–21, until the burst of the property bubble put an end to it. Prominent cases include Guangdong Province and Guangzhou City’s 2-billion-yuan stake in XPeng, as they were aiming to diversify their automotive industry from JVs dominated by Japanese firms.19 Ningbo City also made a 10-billion-yuan investment into Zeekr, the startup project under Geely Group, as the eastern coastal city missed other EV startups in the past decade.20

As discussed earlier, giant automotive SOEs were the early leaders in China’s EV sector. But for most cities, collaboration with these firms has proven unrealistic. As in previous decades, major SOEs have been reluctant to transfer core development and manufacturing capabilities. The political salience of EV production has only reinforced this tendency, as EV development is now a key performance metric for both SOEs and the local governments in their headquarters’ cities. This makes them even less willing to disperse research, development, and production beyond their home bases. SAIC, for example, doubled down on EV development and manufacturing after Xi Jinping’s 2014 visit to the company, during which he stressed that “developing new energy vehicles is essential for China to evolve from an automobile power to an automobile powerhouse.”21 Yet throughout the 2010s, SAIC built no EV development or manufacturing facilities outside Shanghai, except in Ningde, Fujian. Ningde was an exceptional case for three reasons: It is home to Contemporary Amperex Technologies (CATL), the world’s largest power battery producer since 2017; Xi Jinping served there as prefectural Party secretary from 1988 to 1990, earning key promotions from his tenure; and Fujian’s governor from 2018 to 2020, Tang Dengjie, was a long-time senior SAIC executive eager to connect his former company with the province.22

Cities lacking such advantages had less bargaining power with the large SOEs. Changzhou, unable to persuade Dongfeng to produce competitive models until 2018, turned instead to BAIC, another major EV-making SOE. Attracted by Changzhou’s large battery manufacturing base, BAIC began building a plant in the city’s Wujin District in 2015. When production began in 2016, however, the main output was a two-seat city car, marginal in BAIC’s product lineup.23 In 2023, with an annual manufacturing capacity of 300,000 vehicles but weak sales, the BAIC plant shut down. Wujin’s partnership with Li Auto proved more fruitful. Li Auto began constructing its manufacturing base there in 2016 and, despite its Beijing headquarters, produced all of its main models in Changzhou until 2023.24 The company also helped attract key members of its supply chain, including its electric vehicle control system and electric power train manufacturer Inovance and its seat unit supplier Forvia, into Changzhou. By the end of 2024, 32 of Li Auto’s 100-plus suppliers were based in Changzhou, making it Jiangsu’s second-largest automotive supply hub after Suzhou, which has hosted major international tier-one suppliers since the 1990s.25

CONCLUSION

A key driver of China’s rapid growth in both the traditional automotive and EV sectors has been the alliance between local governments and private capital. These partnerships first emerged in the 1990s, when local governments, eager to develop automotive manufacturing, found themselves shut out by restrictive central-level industrial policies. Long-standing structural issues, such as the disparity in bargaining power and misaligned incentives, limited their ability to collaborate with established SOEs. In the 2000s and 2010s, while certain policy restrictions eased, core barriers remained, including JV quotas, manufacturing qualifications, and entrenched SOE favoritism. At the same time, the maturation of China’s capital markets, the proliferation of diverse shareholding structures, the rise of EV startups, and post-2008 credit expansion deepened local governments’ ties with private firms, leading to the proliferation of competitive EV makers and the emergence of new “motor cities” across China.

However, the close local-private alignment has also contributed to structural problems, most notably chronic overcapacity and cutthroat competition. Local investment sprees have produced excess manufacturing capacity in both EVs and ICEVs.26 When automotive startups fail, their close financial and political ties to local governments exacerbate municipal debt problems and slow market exit. These risks are heightened when local governments make strategic investment decisions without adequate due diligence or sector-specific expertise. One notorious example was the partnership between Rugao County in Nantong and Sailin, an EV spin-off from the US sports car maker Saleen. Without thoroughly assessing the firm’s investors, capabilities, or technology, the county invested 6.6 billion yuan in a company that produced almost no cars.27 This is not unique to China: In the United States before the 1930s, hundreds of automakers emerged in a wave of investment fever and overcapacity, although they were geographically concentrated around Detroit and far less dependent on local government backing.28 In China, by contrast, local governments play a pivotal role. Each locality tends to view industrial investment primarily through its own fiscal lens, often prioritizing short-term revenue and regional growth over broader national or global market dynamics. Reflecting these concerns, central leaders in 2025 explicitly warned local governments against blindly launching new EV projects.29

It is worth noting that the technological shift in the automotive sector, particularly the rise of electric and connected vehicles, partly contributed to the alliances between local governments and private capital. These changes created crucial windows of opportunity for weaker actors and new entrants, such as the “internet carmakers,” to enter and compete.30 Similar patterns appeared in other industries. In the EV charger market, which was once dominated by state monopolies (State Grid and China Southern Power Grid), private firms like TELD in Qingdao and StarCharge in Changzhou leveraged mobile connectivity and local government support to become leaders. China’s AI sector shows a comparable dynamic: DeepSeek, spun off from a hedge fund in Hangzhou, thrived under municipal protection even as hedge funds were criticized by some central leaders as financial speculators.

As private capital expanded and China’s capital markets deepened, local governments adapted quickly, forging alliances that frequently outmaneuvered central regulatory constraints. This partnership between local authorities and private capital not only reframes our understanding of China’s industrial development but also offers a powerful lens for anticipating the evolution of high-value manufacturing sectors. In dialogue with the comparative literature on local developmental states,31 this study also provides theoretical and process-tracing accounts of how such alliances are cultivated by local developmental states and how, in turn, they reinforce local developmental capacities.

Localized Bargaining: The Political Economy of China's High-Speed Railway Program

Pekingnology is privileged to share an exclusive excerpt from the new book Localized Bargaining: The Political Economy of China's High-Speed Railway Program, just published by Oxford University Press (and available on Amazon).

Chery was founded in 1997 as the Anhui Auto Part Company, a regional SOE jointly owned by Anhui Province and the City of Wuhu. By 2025, however, the combined provincial and municipal ownership had declined to less than 30 percent.

The “three big” JVs were Shanghai-Volkswagen, FAW-Volkswagen, and Dongfeng-Citroën, while the “three small” were Beijing-Jeep, Guangzhou-Peugeot, and Tianjin Auto (licensed by Daihatsu). In the early 1990s, two additional supermini manufacturers with defense-industry backgrounds, Chang’an-Suzuki and Guizhou Aviation Industry (partnered with Subaru), were admitted. The only major exception to the “three big and three small” policy of the 1990s was Shanghai GM, thanks to Shanghai’s political connections with central leaders such as Jiang Zemin and Zhu Rongji. See Michael Dunne, American Wheels, Chinese Roads: The Story of General Motors in China (Wiley, 2011).

Before the 2000s and the popularization of sport utility vehicles (SUVs), the Chinese term jiaoche (轿车 ‘sedan’) generally referred to all light passenger vehicles, including sedans, hatchbacks, and non-off-road unibody SUVs.

Yuan Jia-Zheng and Carles Brasó Broggi, “The Metamorphosis of China’s Automotive Industry (1953–2001): Inward Internationalisation, Technological Transfers and the Making of a Post-Socialist Mar ket,” Business History 67, no. 1 (2025): 211–38.

Jia Xinguang, 透析车界 [Analyzing the automobile world] (Renmin Jiaotong Chubanshe, 2004), 20–24.

For local state corporatism and local governments’ roles in industrial firms in the 1990s, see Oi, “Fiscal Reform”; Andrew G. Walder, “Local Governments as Industrial Firms: An Organizational Analysis of China’s Transitional Economy,” American Journal of Sociology 101, no. 2 (1995): 263–301.

Qin Shuo and Xiong Yuejia, 工程师之魂:比亚迪三十而立 (1994–2024) [The soul of engineers: BYD’s first thirty years (1994–2024)] (Zhongxin Chubanshe, 2024). BYD’s rail transit systems were deliberately designed to circumvent the approval of the plan for the subway system (PSS) overseen by the National De velopment and Reform Commission (NDRC) and other central ministries, including the Ministry of Envi ronmental Protection and the Ministry of Housing and Rural-Urban Development. For local leaders’ incen tives in developing urban rail transit systems and the PSS in China, see Zhenhuan Lei and Junlong Aaron Zhou, “Private Returns to Public Investment: Political Career Incentives and Infrastructure Investment in China,” Journal of Politics 84, no. 1 (January 2022): 455–69.

Miao Wei, 换道赛车:新能源汽车的中国道路 [Changing lanes to race: China’s path for new energy vehicles] (Renmin Youdian Chubanshe, 2023), 174-77.

Wang Ziliang, 风云纪:吉利收购沃尔沃全记录 [A chronicle of events: A complete record of Geely’s acquisition of Volvo] (Hongqi Chubanshe, 2010); Wang Qianma and Liang Dongmei, 新制造时代:李书福 与吉利、沃尔沃的超级制造 [The new manufacturing era: Li Shufu and Geely-Volvo’s super manufacturing] (Zhongxin Chubanshe, 2017).

Ren Jiao, “马斯克、贾跃亭、李斌们陷造车困境” [Elon Musk, Jia Yueting, and Li Bin face car-making dilemmas], 新京报 [Beijing News], October 15, 2018, http://www.caam.org.cn/chn/1/cate_82/con_5219553.html.

National Development and Reform Commission and Ministry of Industry and Information Tech nology, “新建纯电动乘用车企业管理规定” [Regulations on the administration of newly established pure elec tric passenger vehicle enterprises], 中华人民共和国国家发展和改革委员会 [National Development and Re form Commission of the People’s Republic of China], July 10, 2015, https://www.ndrc.gov.cn/xxgk/zcfb /fzggwl/201506/W020190905494986821080.pdf.

Fengming Lu’s interview with a former government official in Wujin County, Changzhou, Jiangsu, May 21, 2024.

Fang Chao and Shi Yingjing, “新能源汽车过度内卷样本:南京9年5次‘造车梦碎’” [An example of excessive competition in new energy vehicles: Nanjing’s five failed “car-making dreams” in nine years], 中国经营报 [China Business Journal], May 17, 2025, https://www.cnenergynews.cn/news/2025/05/17/detail _20250517213152.html.

Yao Lijuan and Zheng Zhiyan, “新能源汽车生产资质之路在何方” [Where is the road to new energy vehicle production qualification?], 金杜律师事务所 [King & Wood Mallesons], July 23, 2019, https:// www.kwm.com/cn/zh/insights/latest-thinking/where-is-the-road-to-new-energy-vehicle-production -qualification.html.

Fengming Lu’s interview with EV 100 executives, January 15, 2024.

Examples include XPeng’s use of Haima’s manufacturing qualification in Zhengzhou and Li Auto’s reliance on Lifan’s qualification in Chongqing.

For the credit expansion in China after the 2008 financial crisis, see Christine Wong, “The Fiscal Stimulus Programme and Public Governance Issues in China,” OECD Journal on Budgeting 11, no. 3 (2011), https://doi.org/10.1787/budget-11-5kg3nhljqrjl; Longyao Zhang, Sara Hsu, Zhong Xu, and Enjiang Cheng, “Responding to Financial Crisis: Bank Credit Expansion with Chinese Characteristics,” China Economic Review 61 (2020): 101233.

Zeng Le, “从北京亦庄到合肥, ‘流浪’蔚来官宣落户, 项目计划融资超百亿元” [From Beijing Yizhuang to Hefei, “wandering” NIO officially settles, with project financing planned to exceed 10 billion yuan], 亿欧网 [EqualOcean], February 25, 2020, https://nev.ofweek.com/2020-02/ART-71000-8100-30429018.html.

Fengming Lu’s interview with officials of Guangdong provincial government, November 21, 2023.

Fengming Lu’s interview with officials of Ningbo municipal government, June 19, 2023.

Xinhua News Agency, “习近平在上海考察时强调 : 当好全国改革开放排头兵 不断提高城市核心竞争力” [Xi Jinping emphasized during his inspection tour in Shanghai: Serve as the national vanguard of reform and opening-up and continuously enhance the city’s core competitiveness], 人民日报 [People’s Daily], May 25, 2014, 1, https://www.gov.cn/guowuyuan/2014-05/24/content_2686434.htm.

Fengming Lu’s interview with an official of Ningde municipal government, June 10, 2023; Fengming Lu’s interview with a senior executive of Ningde municipal government’s investment fund, June 12, 2023.

Gasgoo News, “北汽新能源汽车发展状况及常州高端产业基地” [Development status of BAIC new energy vehicles and Changzhou high-end industrial base], 盖世汽车 [Gasgoo Auto], March 20, 2018, https://auto.gasgoo.com/News/2018/03/20033752375270037000C601.shtml.

Fengming Lu’s interview with a former government official in Wujin District, Changzhou, Jiangsu, May 21, 2024.

Fan Yicheng, “拉上理想比亚迪, 新万亿之城常州加速转向新能源 F 城市观察家” [Partnering with Li Auto and BYD, Changzhou, China’s new trillion-yuan city, accelerates shift to new energy F City Ob server], 界面新闻 [Jiemian News], March 10, 2025, https://www.stcn.com/article/detail/1572476.html.

Clarence Leong, “China Makes More Cars Than It Needs. Now, It’s Shakeout Time,” Wall Street Journal, January 9, 2025; John Paul Helveston, Paul Triolo, and Jonas Nahm, “The Problem with ‘Overcapacity’ in China’s Automotive Industry,” The Wire China, September 8, 2024.

Su Jiede and Xu Dawei, “江苏赛麟造车大败局” [The great failure of Jiangsu Sailin in Automaking], 中国新闻周刊 [China Newsweek], August 10, 2020, https://finance.sina.cn/2020-08-10/detail-iivhvpwy0138625 .d.html.

John Bell Rae, The American Automobile: A Brief History (University of Chicago Press, 1965).

Du Shangze and Yang Xu,【“ 微观察•习近平总书记在中央城市工作会议上】‘有些事要打攻坚战, 有些 事要久久为功’” [Micro-Observation: General Secretary Xi Jinping at the Central Urban Work Conference, “Some tasks require tough battles, others call for long-term perseverance”], 人民日报 [People’s Daily], July 17, 2025, https://www.gov.cn/yaowen/liebiao/202507/content_7032431.htm. Similar overcapacity issues also existed in other industries that grew out of local competition, such as the steel case noted earlier.

For early examples, see Daron Acemoglu, Simon Johnson, and James Robinson, “The Rise of Europe: Atlantic Trade, Institutional Change, and Economic Growth,” American Economic Review 95, no. 3 (2005): 546–79.

Francis Edward Hutchinson, “‘Developmental’ States and Economic Growth at the Sub-National Level: The Case of Penang,” Southeast Asian Affairs (2008): 223–44; Shen and Tsai, “Institutional Adaptability.”

| A guest post by

|

This is an excellent article, and I strongly agree with its central conclusion: China’s EV boom cannot be understood as a simple story of top-down industrial planning from Beijing. It was built through a much more complex system: central direction, local government competition, private-sector experimentation, supply-chain clustering, and ruthless market selection. The article is especially valuable because it shows that the real engine of China’s EV rise was not only national policy, but the institutional capacity of local China.

This is exactly the framework I discussed in my earlier essay on China’s “local government entrepreneurs.” In China, local governments are not merely regulators or passive implementers of central policy. They often behave like developmental entrepreneurs: mobilizing land, credit, infrastructure, industrial parks, suppliers, talent, and political attention around emerging sectors. The EV industry is one of the clearest examples of this mechanism. Beijing created the strategic direction, but local governments turned that direction into industrial ecosystems — sometimes successfully, sometimes wastefully, but always with extraordinary intensity. That is why China’s EV boom is best understood not as a subsidy story, but as a state-capital-local competition system.

Like it or not decentralization has been a theme in Chinese development:

1. Mao: Let a hundred flowers blossom.

2. Before China’s accession to the WTO in 2001, the country’s automotive sector was characterized by three defining features: high import tariffs on vehicles, an industrial policy favoring large SOEs, and a fragmented production landscape. The first two were embedded in the automobile industrial policies of 1987 and 1994.

3. While most cities were formally excluded from large-scale passenger vehicle manufacturing, many already hosted small-scale producers, a legacy of Mao’s intentional economic fragmentation that accelerated through the early decades of the reform. Three waves of decentralization, the Great Leap Forward, the Cultural Revolution, and the fiscal decentralization of the 1980s, had encouraged provinces and prefectures to establish their own modest automotive works. Although often economically inefficient, these facilities alleviated chronic vehicle shortages under the planned economy, and many survived into the 1990s.

Apart from this there is the Chinese desire to produce, the ability to ' make do' and to innovate.